.png)

Frameworks, core principles and top case studies for SaaS pricing, learnt and refined over 28+ years of SaaS-monetization experience.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

.png)

2026 pricing

.jpg)

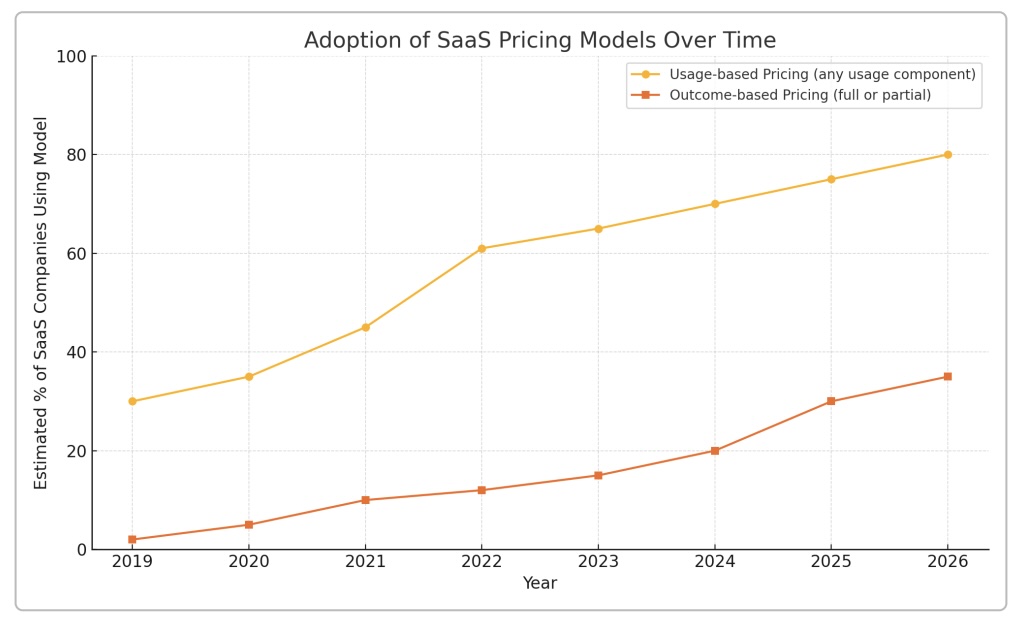

Over the past five years, SaaS pricing models have undergone a quiet revolution. In 2019, the per-user (seat-based) subscription was king – software was typically sold at a fixed price per seat per month or year. But by the early 2020s, usage-based pricing surged onto the scene, aligning price with actual consumption. Industry data shows this shift clearly: by 2022, 61% of SaaS companies were using some form of usage-based model, up from roughly half that a few years prior. This trend toward pay-as-you-go reflected the influence of cloud economics and product-led growth strategies. And on the horizon, an even more radical idea was emerging: outcome-based pricing, where customers pay for results achieved rather than licenses or usage. Gartner projected that by 2025 over 30% of enterprise SaaS solutions would incorporate outcome-based components (up from ~15% in 2022)– a testament to how quickly the conversation was shifting beyond traditional models.

Adoption of usage-based and outcome-based pricing models in SaaS, 2019–2026. Usage-based pricing (yellow line) became mainstream by 2022 (61% adoption), while outcome-based models (orange line) are nascent but expected to reach ~30% adoption by 2025. (Data: OpenView, Gartner)

What drove this evolution from per-seat to usage to outcomes? Several converging forces changed how SaaS companies package and charge for value:

Fast-forward to 2026, and we find ourselves in a paradoxical situation. On one hand, the pricing innovation of the early ’20s continues – more companies have usage-based and value-based pricing than ever. On the other hand, market forces are emerging that just might swing the pendulum back toward simpler models. To unpack this, we need to consider how deflationary technology trends are colliding with the slow pace of change in business practices.

Futurist Brian Roemmele has argued that advanced AI will ultimately drive the cost of software to effectively zero – making it “free like water.” This isn’t as far-fetched as it sounds. Software has long been the most deflationary product category in tech: it massively increases efficiency while its distribution cost approaches zero. Even before the AI boom, investors and analysts recognized that “software is a great deflationary weapon” for businesses, as it cuts costs and boosts productivity (hgcapital.com). In other words, software inherently delivers more for less over time. Mark Billige of Simon-Kucher noted that software drives efficiency and takes cost out, so in an inflationary world you can justify software prices by the savings they generate (hgcapital.com). Now add AI to the mix, and the deflationary effect goes into overdrive. AI can take tasks that used to require a full-time employee and perform them in seconds for pennies – if that. Roemmele points out that we are living through possibly “the largest deflationary moment in history”, as AI and automation make raw intelligence and labor abundant and cheap (x.com). When something becomes abundantly available, economics tells us its price falls accordingly. The marginal cost of software services powered by AI is trending toward nil, aside from infrastructure electricity and chips (which themselves are getting cheaper relative to compute power).

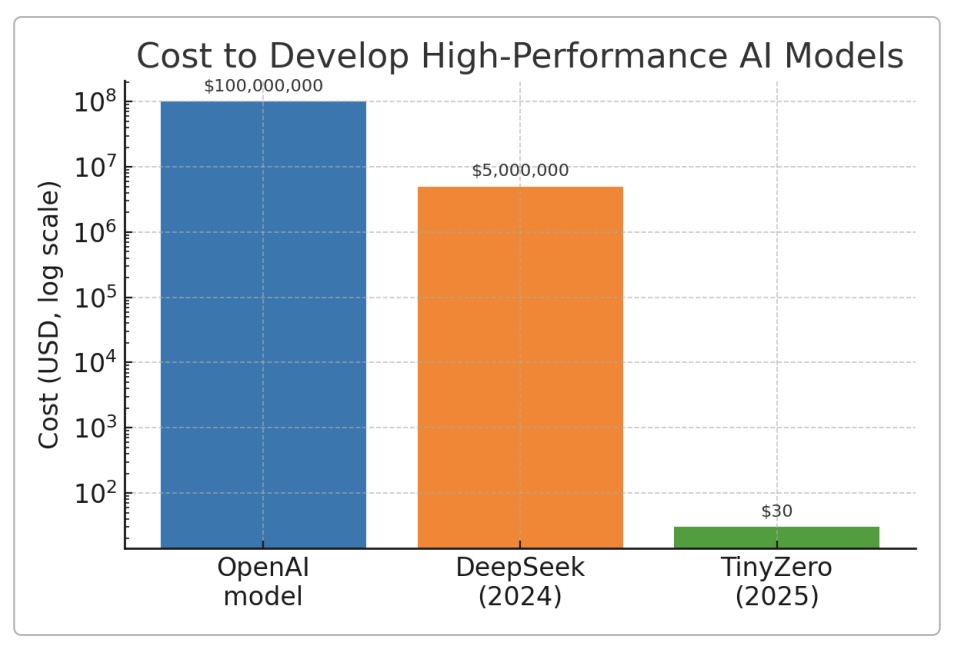

A striking example: in 2024 a cutting-edge AI model might have cost millions to develop, but by 2025 researchers recreated a similar model for only $30 of compute. Such jaw-dropping cost collapses (over 99.99% cost reduction in that case) illustrate how AI tech is commoditizing rapidly. The chart below visualizes one such case – OpenAI’s proprietary model (estimated ~$100M cost) versus a 2024 Chinese model “DeepSeek” ($5M) versus the 2025 Berkeley “TinyZero” reproduction ($30):

Dramatic deflation in AI costs: Cost to develop high-performance AI models has plummeted, as seen by the drop from ~$100M to build a top model (OpenAI) to $5M (DeepSeek) to just $30 (TinyZero). Log scale used on the vertical axis.

With AI cost curves like this, Brian Roemmele’s vision of essentially free software utilities starts to feel plausible. Software was already deflationary; AI is making it exponential. One might expect this to completely upend pricing – if software tends toward free, how do you charge for it at all? Roemmele’s implication is that AI will make basic software capabilities as cheap and ubiquitous as water or air. For SaaS vendors, that raises an ironic situation here in 2026: while many have been busy shifting from seat licenses to usage and outcomes, the declining cost of providing the service could undermine the very rationale for those complex models.

Here’s the paradox: enterprises have only gradually embraced these new pricing models, and many are still most comfortable with simple, predictable pricing like per-seat subscriptions. At the same time, AI-driven cost deflation means vendors might be able to afford simplicity again. If the cost to serve each user drops dramatically thanks to AI optimizations, charging per user (regardless of usage) could remain profitable for vendors and very attractive to customers. We’re already seeing hints of a seat-price resurgence. Some SaaS CEOs in the early 2020s learned that customers “didn’t want innovative pricing” so much as they wanted a familiar, budgetable model. For example, the CEO of Kustomer (a customer support SaaS) initially considered a consumption model but discovered that buyers preferred the old-school per-seat approach that mapped to the budgets they already had for Zendesk, etc.. That lesson resonates in 2026: many clients have been slow to adjust their procurement habits. They still often ask, “How much will it cost per user?” or “What’s my flat annual fee?” In complex enterprise sales, a straightforward per-seat or flat-rate proposal is easier to swallow than a metered usage contract with unpredictable bills.

Thus, the stage is set for an ironic twist. Just as everyone proclaimed usage-based pricing the future of SaaS, and as AI’s high infrastructure costs originally pushed pricing toward usage-based models, the very success in cutting those costs could allow a pivot back to simpler pricing. In 2026 we may see the pendulum swinging back: some SaaS providers reintroducing seat-based packages or tightening the caps on usage-based plans to make costs more predictable. In sectors where AI has slashed COGS by an order of magnitude, a vendor can offer a flat per-user fee that undercuts competitors’ complicated usage pricing – essentially betting that their AI efficiencies make the economics work. After years of complexity, a return to elegant simplicity has appeal.

None of this is to say usage-based or outcome-based pricing will disappear – far from it. Rather, we’re likely to see hybrid pricing dominate this transitional era. Think base subscriptions with usage allowances, or per-seat pricing that includes “fair use” limits instead of pure all-you-can-eat or strictly metered plans. The monetization strategy becomes a balancing act: embrace new models enough to align with value, but not so much as to alienate customers or complicate the sale. And as AI makes software delivery cheaper, companies can afford to be more generous with usage in each seat license, alleviating the need to nickel-and-dime customers on consumption. The paradox of 2026 is that while software is cheaper than ever to provide, software pricing is more of a patchwork than ever – a mix of legacy models and cutting-edge ideas, all coexisting. As we’ll see next, the advent of agentic software is a big reason why this pendulum is swinging in multiple directions at once.

One of the buzziest concepts in 2026 is “agentic” software – AI-driven software agents that perform end-to-end tasks autonomously. Unlike traditional apps that are tools for a user, these AI agents are the user, in a sense, acting on behalf of humans. They don’t just assist with one step; they can plan, execute, and iterate on goals across an entire workflow. For example, an AI marketing agent might write, test, and optimize campaigns continuously until certain conversion targets are met, or an AI support agent might handle every incoming ticket and only escalate issues if absolutely needed. In short, agentic software delivers complete outcomes, not just features. Your marketing AI doesn’t charge you per email sent; it aims to deliver increased conversion rates. Your support AI doesn’t bill by message; it promises to keep customer satisfaction above 95% by resolving issues autonomously.

This shift to AI agents changes the pricing calculus dramatically. If an AI sales agent can book meetings just like a human SDR (sales development rep), how should you price it? By the “seat” (even though it’s an AI, not a person)? By usage (per call or email it makes)? Or by outcome – e.g. a fee per qualified lead or meeting it delivers? Many startups are opting for the outcome route, essentially charging for the results the agent produces. Monetizely’s approach to agentic AI pricing echoes this: tiers could promise pricing “per qualified lead,” “per issue resolved,” or even a flat monthly fee tied to guaranteed KPI thresholds, with bonuses for exceeding targets. This outcome-centric pricing makes the value tangible – it says to the customer, “We get paid when you get X.” It’s the ultimate value-based model, and it aligns well with the nature of AI agents.

However, in practice, we are seeing a pricing reversal or pendulum effect as companies navigate this new terrain. Initially, one might think agentic software would push everyone firmly into outcome-based pricing (after all, if the agent delivers a complete outcome, why not charge that way?). But real-world business dynamics are messy. Vendors and customers are in a learning phase with AI agents. There’s uncertainty around how to measure outcomes fairly, how to contract for them, and how to account for factors outside the AI’s control. As a result, many companies are retreating part-way back to simpler models while the kinks get worked out.

In 2024, venture capitalist Tom Tunguz mused on three possible models for AI agent software: (1) charging a much higher per-seat price (e.g. triple the price, if the AI makes one “agent seat” as productive as three humans), (2) true usage-based pricing (charge per compute resources or queries, akin to how databases charge), or (3) pure pay-for-performance (e.g. per meeting booked) Each approach has pros and cons. Interestingly, Tunguz noted that introducing these models would be a shock to customers used to SaaS, and that it “will take time for both vendors & customers to grasp the implications”. We are living that transition period now. The pendulum is swinging, but not in one clean motion.

What’s happening in 2026 is a hybridization and partial reversion in pricing for agentic software:

The Kustomer anecdote mentioned earlier is instructive here again: customers often say they want innovative pricing that matches value, but they also greatly value predictability and familiarity. In the case of Kustomer, sticking to a conventional seat-based model helped win over mid-market clients who had fixed budgets for helpdesk software. Similarly, here in 2026, we see agentic AI companies sometimes advertising old-school pricing options (“flat monthly license” for your AI agent) to reduce buyer anxiety. It might feel like a step backward from a technologist’s perspective, but it can be a smart go-to-market move during the adoption phase of a disruptive product.

In summary, agentic AI is pushing the boundaries of what software does and thus how it can be monetized. We’re likely in for a rollercoaster: initial excitement leading to exotic outcome-based pricing experiments, followed by a practical rebound to hybrids or even premium seat models to make sales frictionless, and eventually, once AI is trusted and pervasive, maybe another swing toward more radical models. It’s a reminder that pricing models often zigzag rather than progress linearly. The “best” model is a moving target, influenced as much by customer psychology and sales logistics as by pure value alignment.

Peering a bit further out, one can imagine a future where AI-driven systems handle entire business functions – a future where the software essentially becomes the workforce. In such a scenario, outcome-based pricing might seem like the logical end state: if the AI is your sales team, maybe you just pay for deals closed; if it runs your accounting, you pay per report or per compliant month, etc. However, even in this hypothetically AI-saturated future, there are structural limits to outcome-based pricing. Pure outcome-based models run into challenges that likely cap their adoption without significant human partnership (a “services layer”) alongside the software.

What are the inherent limits of charging purely for outcomes?

Because of these factors, the consensus among many industry thinkers is that sustainable outcome-based pricing will likely be a hybrid of software + services. The software provides the automation, and a layer of human experts ensures the outcomes and handles the unexpected. The pricing then might be structured as a subscription plus performance bonuses or usage fees – reflecting that mix of product and service. In fact, the current trend is exactly that: hybrid models as a pragmatic compromise. They allow both vendor and customer to dip their toes into outcome-based value sharing without betting the farm on it. For example, a SaaS might charge a base fee and offer a partial refund or credit if certain targets aren’t met (a form of outcome guarantee). Or they might have tiers where hitting certain metrics unlocks better pricing for the customer. All of these require the vendor to take on some service-like responsibilities (customer success involvement, etc.), reinforcing the idea that pure automated outcomes aren’t a set-and-forget sale.

The bottom line: even in an AI-eats-jobs future, pricing won’t fully escape the need for human touch. Outcome-based models will reach natural limits unless paired with service elements that ensure the promised value is realized. The likely end state is not a binary “outcomes or bust” scenario, but a continuum of models. SaaS companies will position themselves along this continuum based on their product’s nature and their customers’ preferences. Some will lean more into being outcome-delivery partners (almost like outcome-as-a-service, with significant service components). Others will package AI automation as traditional software subscriptions because their market simply isn’t ready to transact on outcomes. The diversity of business needs and comfort levels means one size won’t fit all – and that’s okay.

If there’s one thing to take away from the evolution of SaaS pricing up to 2026, it’s that pricing models are cyclical, not linear. We’ve seen them evolve, revert, and hybridize in response to technology shifts and customer psychology. The journey from per-seat to usage-based to outcome-based has not been a straight line of progress, but rather a series of oscillations – each new model solving some problems while introducing others, leading to the next adjustment. As Mary Meeker might put it in an Internet Trends report: the data shows innovation in pricing, but also the inertia of tried-and-true models. As Tom Tunguz might blog in a conversational tone: the best pricing strategy is the one that balances value capture with customer acceptance, and that balance is a moving target.

One constant force underlying these shifts is the deflationary arc of technology. Software has continuously delivered more value for less money over time, pressuring vendors to either lower prices or deliver correspondingly more value. AI is now accelerating that deflationary trend in dramatic fashion. As noted, SaaS prices historically almost always deflate over time, requiring companies to adjust packaging and innovate to stay relevant. We’re seeing that in real time – the cost of AI capabilities is plummeting, and in response, pricing strategies are adjusting across the industry. In some cases, prices are literally coming down or flattening; in others, vendors are adding more value into each dollar of price (for example, bundling more features or service at the same price point) to avoid outright price drops. Either way, the long arc of tech deflation bends toward lower costs and democratization of capability, which inevitably shapes the economics of software.

Importantly, “lower cost” doesn’t automatically mean “completely free” – but it changes where the money is made. Software might become “free like water” at the point of use, with revenue coming from elsewhere (services, premium features, or simply higher volume of users). We’ve seen analogous trends in tech before: search engines and social networks became free to use (monetized by ads), many developer tools went open-source (monetized by support or cloud hosting), etc. AI software could follow a similar pattern, especially if Brian Roemmele’s vision holds and the marginal cost of intelligence drops to near-zero. Perhaps basic AI-driven software becomes a virtually free commodity, and the service and expertise around it is what customers pay for – a potential future where pricing is for “water delivery” rather than the water itself.

For SaaS leaders reading this in 2026, the key is to stay flexible and attuned to customer perceptions of value. We’ve watched the cycle: from simple to complex (seat to usage), and now a partial swing back to simplicity (hybrids and simpler constructs) under new constraints. Don’t be surprised if in a few years, another swing occurs – for example, if a recession hits and CFOs mandate simpler fixed pricing, we could see a broad reversion to subscription models; or if AI truly becomes cheap as water, we might see entirely new “all-you-can-benefit” pricing emerge. The smart strategy is to build pricing architecture that can evolve – much like software architecture – without alienating your customers.

In closing, the pricing of SaaS in the age of AI is a story of evolution and equilibrium-seeking. Each model (per-seat, usage, outcome) had its day in the sun and its reckoning in the shade. The industry learned that no single model is universally best – it depends on the product, the buyer, the economic context. What is universal is the pressure of technology’s deflationary economics pushing us forward. SaaS companies will continue to find inventive ways to charge for value even as that value becomes ever cheaper to provide. Pricing models will keep cycling, remixing, and reinventing themselves. But if you zoom out, the long arc bends toward greater value for the customer’s dollar – an inevitable outcome of tech progress. And in that sense, yes, software (with a big assist from AI) truly is becoming “free like water” – or at least, freer, more abundant, and more essential – changing the business of software in ways we are only beginning to fully grasp.

Ultimately, navigating these pricing cycles requires both analytical rigor and empathy for the customer. Price to what the market will bear and what the market will embrace. Keep an eye on costs and an ear to the ground. The 2026 guide to SaaS pricing isn’t a final chapter, but a snapshot in an ongoing story. If history is any guide, the only sure prediction is that in a few years we’ll be writing yet another chapter, reflecting on how today’s models evolved yet again. And that’s the exciting part – pricing, like technology, never stands still. It’s all about riding the waves of change without losing balance, ensuring your business and your customers prosper together on the long journey ahead.

Sources:

Join companies like Zoom, DocuSign, and Twilio using our systematic pricing approach to increase revenue by 12-40% year-over-year.